Kraft Heinz (KHC): Berkshire Brand

Perspectives, by Mark Robertson, Managing Partner September 14th, 2023

Anticipation? In the realm of hot dog consumption, "Are you an animal?" Morningstar cites Kraft Heinz (KHC) as a Berkshire Hathaway holding and suggests a favorable outlook for this culinary staple. Do you agree? By the way, the answer is 42. This summary provides a closer look at the pieces of the Equity Analysis process.

Undervalued by Nearly 40% and Yielding Almost 5%, This Stock Is a Buy — Is It?

It’s a Warren Buffett stock pick, too.

The third-largest food and beverage manufacturer in North America, Kraft Heinz KHC has been a longtime holding of Berkshire Hathaway. In fact, we recently included this dividend stock as one of our three Warren Buffett stocks to buy. Kraft Heinz is also among our analysts’ 33 undervalued stocks for the third quarter. It’s one of Morningstar chief U.S. market strategist Dave Sekera’s five undervalued dividend stocks to buy, as well.

Kraft Heinz benefited from consumers eating at home during the pandemic, with 85% of its sales driven through the retail channel. However, we attribute its more recent performance to its revamped strategy rather than the macro and competitive backdrop. CEO Miguel Patricio has charged the company to pursue lasting efficiencies, increase spending on marketing and product innovation, enhance category management and e-commerce, and leverage its scale to more nimbly respond to changing market conditions. The company targets $2.5 billion in efficiency savings through 2027 and a 30% increase in marketing spending between fiscal 2020 and 2024, which we think stands to support its brand mix and its retail relationships. It also has narrowed its stock-keeping unit count by 20% in North America in the past couple of years. We forecast research, development, and marketing spending to amount to 6% of sales annually on average over the next 10 years, or around $1.9 billion, up from a 4.5% average over the last five years. (Morningstar)

Reference: https://www.morningstar.com/stocks/undervalued-by-nearly-40-yielding-almost-5-this-stock-is-buy

Equity Analysis (KHC)

Undervalued By 40%?

They could be right … but the price-to-fair value ratio of 63%, based on a fair value of $53 seems a little suspect.

Morningstar does a discounted cash flow analysis to determine fair value. A lightning round approach to the same determination is simply to answer the question, “What current price would generate a 8-10% annualized total return?”

Answer: $42

Using $42 as a fair value, the price-to-fair value (P/FV) increases to approximately 80% … a condition that would result in Kraft being “half as much on sale.”

The analyst consensus (ACE) fair value is $38.88 for a P/FV of 86% and would be more in alignment. Keep in mind that we generally observe an extra packet of optimism when it comes to the ACE fair value calculations. It’s as if they work in a Sales Department … or something. [grin]

So a closer look at the milestone assumptions is in order.

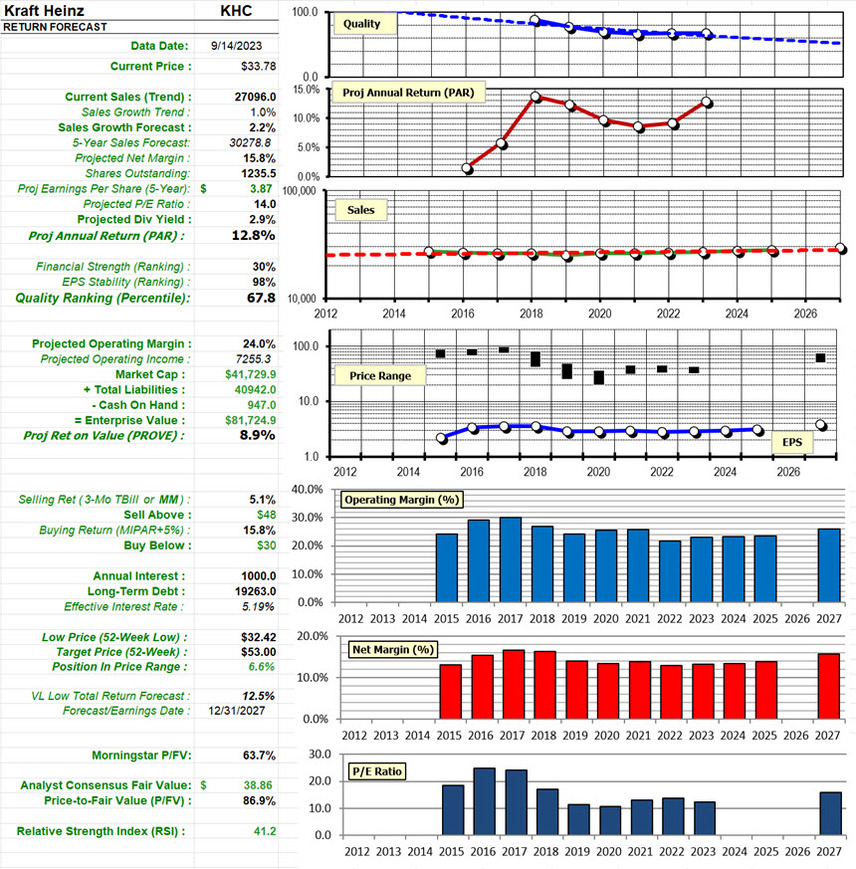

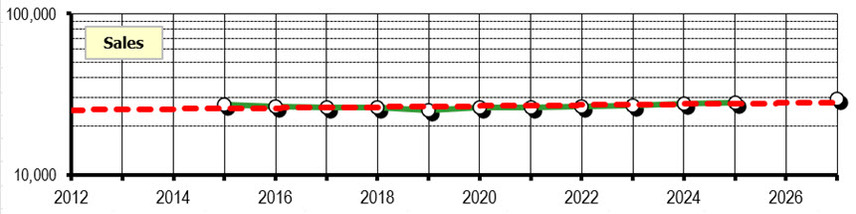

Growth Forecast

Longer term, we forecast 2% average annual sales growth and operating margin holding in the low 20s, which aligns with management’s long-term targets for 2%-3% organic sales growth … (Morningstar)

Value Line is projecting 2% sales growth for the 3-5 year forecast.

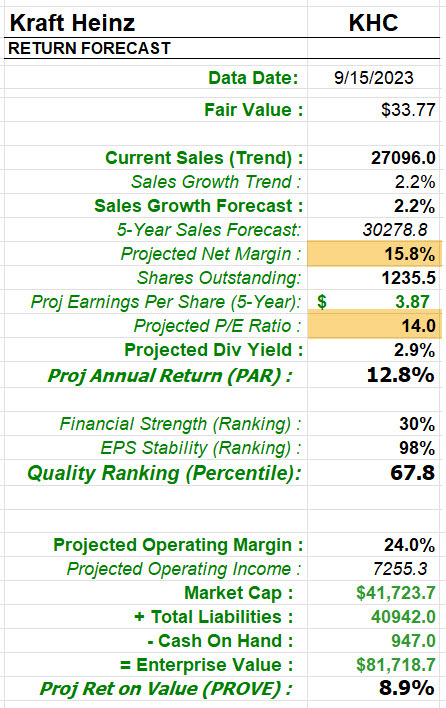

The growth trend for 2022-2027 is 2.2%.

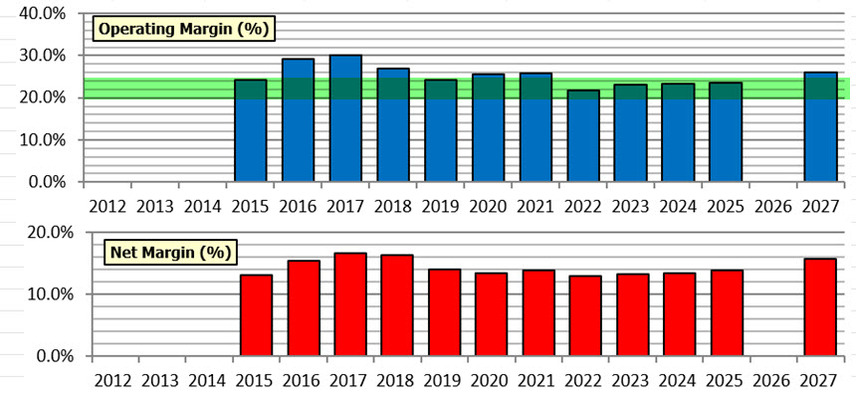

Profitability Outlook

Kraft is definitely a stalwart when it comes to margins, whether of the operating income (PROVE) or net margin, EPS-based (PAR) variety.

As mentioned before, Morningstar is projecting operating margins to remain in the low 20s and this is supported by the accompanying figure.

Value Line has a projected operating margin of 26%, so they’re moderately more optimistic here.

The Value Line net margin forecast is 15.8%, beckoning back to levels last seen in 2017-2019. Morningstar describes an incremental commitment to research & development that would have to succeed for the higher net margins to materialize. If it’s my study, I’m probably closer to 13% on the net margin forecast. But I don’t put ketchup on hot dogs. I am not an animal.

Valuation, Projected Annual Return & Projected Return on Enterprise Value (PROVE)

The implied EPS growth forecast is approximately 6%. Value Line concurs.

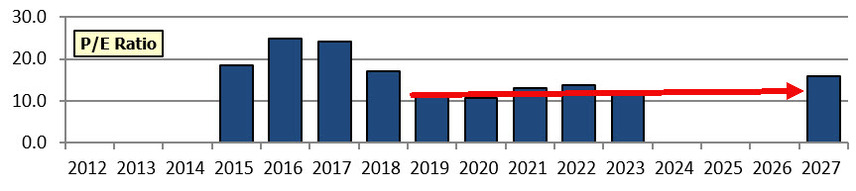

Our valuation implies a fiscal 2024 enterprise value/adjusted EBITDA multiple of around 14 times. (Morningstar)

A price-to-earnings ratio (P/E) will be greater than an “EBIDTA multiple”, so we can assume that Morningstar should/could be using a P/E of approximately 18-19×. The Morningstar fair value P/E is 15.3×.

The trailing 5-year average P/E is 12.2×.

The Value Line 3-5 year forecast P/E is 16×.

The Manifest Investing consensus P/E forecast is 14x and a return to the P/E ratios of 2016-2018, or 22x, seems a low probability.

The Projected Annual Return using 2% sales growth, 13% net margins and a P/E ratio of 14x would be: 8.4%

The PROVE calculation is both an audit and for some, a preferred method that encapsulates the expectations for operating profits while including a look at enterprise value — effectively accounting for capital strategy and balance sheet realities, etc.

Using an operating margin of 24%, that 2.2% top line growth, the current market cap, total current liabilities and cash in the Heinz coffers/wallet, the Projected Return on Value (PROVE) is 8.9%.

- Yes, Virginia, that IS a Stock Selection Guide-based implementation of the preferred procedure … or business model analysis.

- A difference between PAR and PROVE can/should be explored.

- In this case, the 2% sales growth is pretty solid. Any analysis should well consider whether the net margin forecast (15.8%) or the projected P/E ratio (16x in the case of Value Line) should be explored. Based on the accompanying profitability trends in the image, I’d have to discover some deeper drive for margin enhancement before I’d a net margin of 15.8% versus 13% (for example).

Why the below-average Financial Strength?

Yes, Value Line gives them an “A”. But the effective interest rate is 5.19%. That’s NOT an “A” from the people who care about getting paid back. Heinz also has a debt load of $19.3 Billion. When that is scaled versus enterprise value and ranked among all of the companies in our coverage, that component of financial strength would rank in the 23rd percentile.

Bottom line? Great products. We love Pittsburgh. Great people. We still dream of Punxsutawney. I still don’t put ketchup on hot dogs. The current price is attractive, just not as seemingly attractive as the headline. No, I don’t believe Warren Buffett edited the headline.

Mark Robertson

Mark Robertson is founder and managing partner of Manifest Investing, a source for research and portfolio management focusing on strategic long term investors.