Harvesting The January Effect

Funds & Featured Portfolios, by Mark Robertson, Managing Partner December 1st, 2018

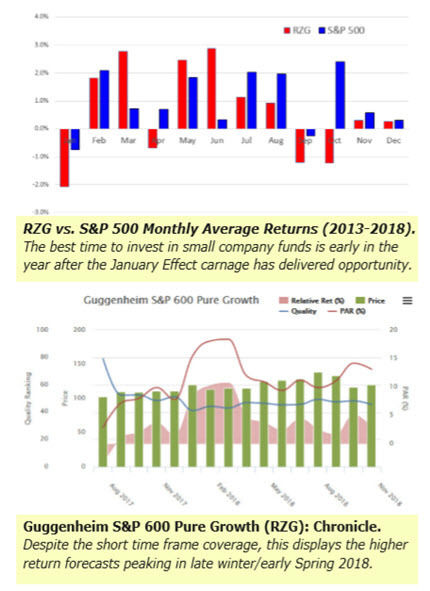

As we've suggested before, the January Effect is real and starts in September and/or October. This anecdotal look at Invesco S&P SmallCap 600 Growth reveals the period of opportunity created by tax-related selling and its impact on smaller companies.

There aren’t too many exchange-traded funds (ETFs) on the leader board for the funds that qualify for our best small company funds. But ranked in the same neighborhood as our favorites Brown Small Company (BCSIX) and T. Rowe Price New Horizons (PRNHX) comes Invesco S&P SmallCap 600® Pure Growth (RZG).

The January Effect is real. As shown here in the accompanying chart, the monthly returns for RZG for the trailing five years have been weakest from September through January. The strongest performance spans February through August when capital apparently chases back into the smaller companies. The accompanying chronicle for the last 1 1/2 years also displays a peak in the overall return forecast back in early 2018 and the PAR has been edging “north” during the current beat down on small companies.

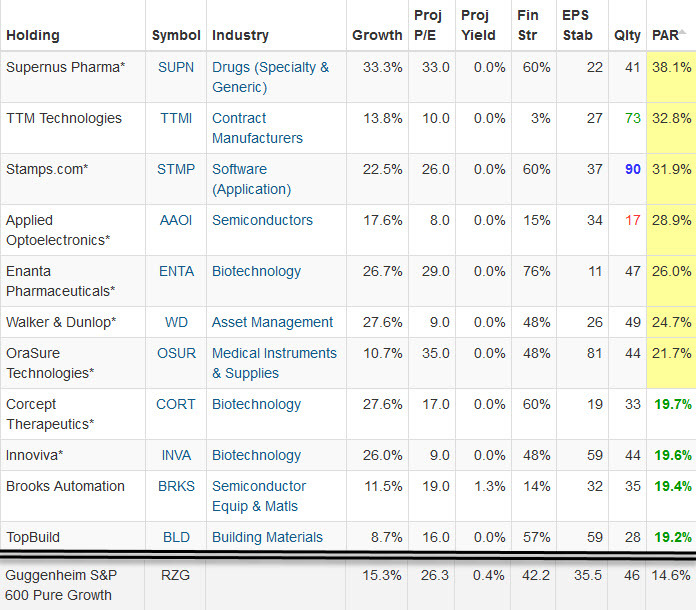

The dashboard excerpt displays the types of companies that Invesco has deemed worthy for this actively managed ETF and we see companies like Stamps.com (STMP) that qualified for our 2019 Best Small Companies as well as others that were candidates. Walker & Dunlop (WD) was one of the better selections made at the NAIC national convention stock selection panel a couple of years ago.

The last five years have been a little lackluster but the 10-year relative return is +2.2% putting the fund among the 20 best performing funds since 2008. The 15.3% average growth forecast is robust and the 14.6% PAR is among the ten best fund return forecasts at this time.

Invesco S&P SmallCap 600® Pure Growth (RZG): Holdings. This dashboard has been sorted (descending) by Projected Annual Return (PAR) and it provides a display of the type of investments made. Average sales growth forecast is 15.3% and the early life cycle characteristics of many of the holdings result in financial strength (42) and quality (46). The overall PAR (14.6%) is on the leader board short list.

Mark Robertson

Mark Robertson is founder and managing partner of Manifest Investing, a source for research and portfolio management focusing on strategic long term investors.