Preserving Capital AND Capital Gains

Cover Story, by Mark Robertson, Managing Partner June 16th, 2017

We think CAPITAL PRESERVATION and CAPITAL GAINS PRESERVATION both matter. This article provides an update of recent explorations and findings with respect to building a better selling discipline based on the time-honored precepts of the modern investment club movement.

While serving as Senior Contributing Editor for Better Investing, Editor Don Danko and I would receive frequent, polite, but persistent pleas for more articles and learning opportunities on selling stocks from a subscriber in New York. The correspondence came like clockwork and Don meticulously thanked him for each nudge. When we published “When To Sell: The Challenge of Reason” (September 2004) he offered to send a gift card for a steak dinner on him. At the National Association of Investors Convention in Cincinnati during May, there were at least five sessions focused on selling decisions and portfolio management. Last year, we started an exploration into some selling decision methods, using our monthly Round Table webcasts as proving grounds. Make no mistake. This is still a work in progress. With incremental promise …

We started scratching our heads over a year ago about this. Our prelimary findings were presented in AND the “Rule-of-5.”

We think CAPITAL PRESERVATION and CAPITAL GAINS PRESERVATION both matter.

No time-honored selling disciplines change with the exploration/concept described here.

We don’t want to give the impression that any of the time-honored selling disciplines change with the exploration/concept described here. We still believe that the reasons for selling are short and simple:

(1) You need the money.

(2) Quality Degradation.

(3) Make the Portfolio BETTER.

Rule One: Make It BETTER

While reviewing all forms of literature on the subject of selling stocks and portfolio management, Ken encountered a number of references by George Nicholson to “Rule One.”

It begged the obvious question, “What is Rule One?”

“Rule One will probably account for 90% of your sell transactions.” – NAIC Investors Manual, September 1, 1984; First Edition.

Rule One: “Sell because an issue of equal quality offers more gain prospects on the upside and apparently less risk on the downside.”

This is precisely what we’ve done for years — a concept recognized by many of as “Challenging” a portfolio. The standard practice is to place the stock with the lowest return potential (lowest PAR) on the “hot seat.” After auditing and updating and debating the merits and future potential for the stock, the evaluation shifts to deciding if the low potential stock can be sold and replaced with an equal or better quality stock with a higher PAR. The proceeds from sale can be invested either “inside the portfolio” with an existing qualifying holding or in a promising new holding.

It’s also the foundation of our “sand boxes” where what-if scenarios for portfolios/dashboard can be explored. As shown on the top half of the accompanying figure, the worksheet for the Round Table tracking portfolio has been sorted by PAR ascending — so the companies appearing at the top of the list (particularly if their return forecast is less than the market average) can be assessed. In this case for a recent webcast, Coach (COH) was in the hot seat.

A Few Moments About “Core”

It makes sense to treat holdings differently, with different expectations and boundaries. We believe it makes sense to hold a core holding (so long as the overall portfolio is OK) until the return forecast dips below money market rates. For a non-core (speculative, turnaround, low-quality company with improvement potential, etc.) we’re inclined to sell if the PAR drops below the average return forecast.

This leads to a definition of core versus non-core. It’s something open to debate. In this context, we believe a core holding is high-quality, with an established track record that has survived at least one recession.

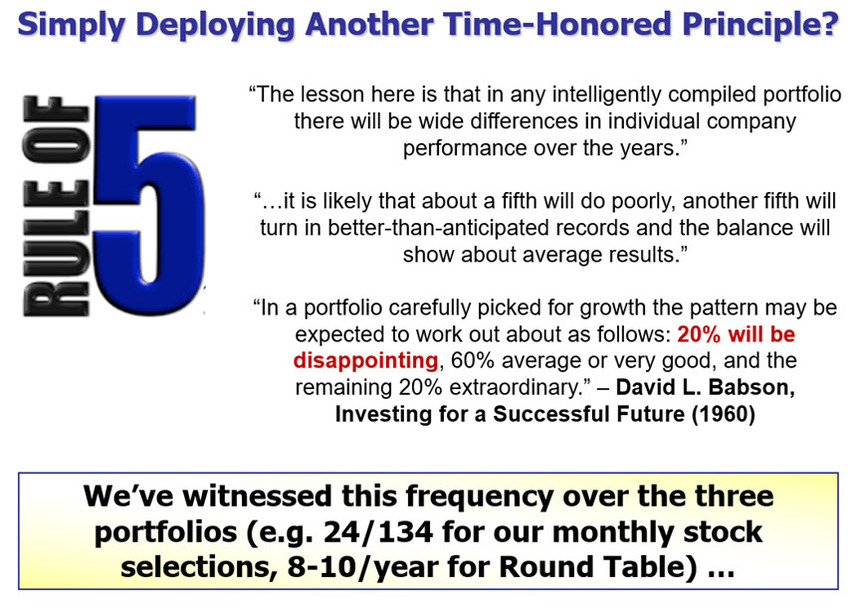

Nudges: Rule-of-Five

We believe that protecting CAPITAL by heeding the Rule-of-5 during the early holding period is logical and potentially very rewarding. We’ve all experienced that stock selection where the story is good and all influences and trends seem to be headed in the right direction. And then, no matter how thorough our study, the wheels come off.

One of the more powerful findings or realizations that we’ve made is that we’re simply defining the Rule-of-5 “disappointments” so we can give them a “time out.” We do this by monitoring the relative return for positions with a holding period less than a year. For more on relative return, see: PAR and quality … and check for industry trends as part of this developing process.

We think the potential is promising. Probably at least as compelling (so far we’ve seen incremental gains in annualized rate of return of +1-3% for the three case studies) as embedding the analyst estimates in our business model analyses. We are here for the returns and it’s the bigger picture, the cumulative results that matter. We’ll continue to test other portfolios and implement standing procedures that may become disciplines and best practices over time.

We’ll explore this capital preservation and rate of return potential enhancement and decide if it’s a worthy improvement in our arsenal.

Our Round Table webcasts are currently scheduled for 8:30 PM ET on the last Tuesday of the month. Join us and help us explore and get better, together.

Mark Robertson

Mark Robertson is founder and managing partner of Manifest Investing, a source for research and portfolio management focusing on strategic long term investors.