We Don’t Need Another Hero

Cover Story, by Mark Robertson, Managing Partner August 1st, 2013

Stock market corrections, recessions and bear markets are no fun. And there is no crystal ball.

Out of the ruins, out from the wreckage

Can’t make the same mistake this time

I wonder when we are ever gonna change it

Living under the fear till nothing else remains

We don’t need another hero

We don’t need to know the way home

Looking for something we can rely on

There’s got to be something better out there

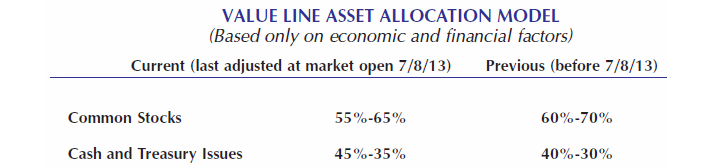

Jeff Traeger noticed and shared something of an epic moment on the Manifest Investing Forum a couple of weeks ago. Value Line raised their commitment to “cash equivalents” to 40% (from 35%) during July. These shifts in guidance are rare and a bit “tectonic”, the last adjustment coming on April 2, 2012. We also noted that one of our favorite market barometers, the median Value Line Low Total Return (VLLTR) forecast has dipped near historical lows (4.5%) last week. Shelly Stokes noticed coverage of another similar Value Line metric (VLMAP) and shared that she was “becoming more convinced than ever that [protective] cash is possibly a good idea.” Sunil Veluvali asked for a summary…

The lyrics are from Tina Turner’s classic. The theme is written from the perspective of those being oppressed and not wanting to get their hopes up in yet another “hero” who may or may not save them. Stock market corrections, recessions and bear markets are no fun. And there is no crystal ball. But we’ll debate Tina on the merits of her argument. While we agree that we don’t need another hero in the form of yet another guru/pundit/talking head, I think we need be our own heroes while extracting lessons of history and knowing the way “home.” For many of us, preservation of capital is important. Not only that, prudent allocation offers the potentially of incrementally superior returns. What are cash equivalents? How does an investor decide what and when to take action? Are there barometers that we can rely on?

Can’t make the same mistake this time … How many of us are weary of the roller coaster of buying a particular stock (or group of stocks) and riding them to a peak or apogee — only to hang on, white-knuckled, while they plummet into the depths? Our own Tin Cup model portfolio remains fully invested at all times and serves as an example of one such roller coaster. We’ve talked about “getting back to even.” (See Tin Cup update, April 2010) Is there something we can rely on?

Time for Timing?

But our community of investors really doesn’t attempt to “time” the market, right? And what about that long-held advice to investment clubs that they remain fully invested at all times?

Value Line Low Total Return (VLLTR) Forecast vs. Actual Results. Mark Hulbert recently featured our monitoring of this relatively reliable market indicator in his Wall Street Journal feature and CBS MarketWatch. Prudent selectivity is more challenging than usual these days.

“Don’t give me timing, give me time.” — Jesse Livermore

Jesse Livermore is regarded and hailed as one of the most successful traders of all time. He also said, “There is a time for all things, but I didn’t know it. And that is precisely what beats so many men in Wall Street who are very far from being in the main sucker class. There is the plain fool, who does the wrong thing at all times everywhere, but there is the Wall Street fool, who thinks he must trade all the time. Not many can always have adequate reasons for buying and selling stocks daily – or sufficient knowledge to make his play an intelligent play.”

A colleague of Joshua “Reformed Broker” Brown shared, “I am never fully invested. There are reasons for this relating to risk management … [this] is about opportunity and the absolute, no exceptions, rule I have, that has served me well, to be ready with ammunition when opportunity arises. I never have to raise cash because I am never fully invested. Ever. Usually, [cash] is 20% of my portfolio but sometimes it is more.”

Valuation Bubble? Many of the aggregate return forecasts that we follow are “subdued.” We don’t pretend to “call” market disruptions, we merely observe/believe that vulnerability to corrections increase as our return forecasts decrease. The fact that many forecasts are predicated on higher multiples (compared to recent history) is NOT EXACTLY a source of great comfort.

Speaking of The Reformed Broker, he’s (as usual) more direct: “All-In is a stupid investment posture, so is All-Out.”

Are the two schools of thought really at odds with each other? Not really. As with many things “investing,” it comes down to a matter of context. In this case, the main consideration is time horizon.

In the case of the modern investment club, what is the theoretical time horizon or duration? Answer: Infinity. (At least in theory) This being the case, a club can choose to remain relatively fully-invested, not unlike our Tin Cup model portfolio. This is also true for relatively young investors with long-term risk tolerance. Timing is something that can be generally disregarded if so desired.

If you’re a human investor, you likely have a finite time horizon and each and every one of us has resource needs that could make capital preservation a very important consideration. George Nicholson allowed for this in some detail in his teachings, stipulating that it was fair and reasonable for investors to allocate between core holdings, non-core holdings and “cash equivalents” when conditions merit and to support the pursuit of the opportunities suggested by Jesse Livermore. History does repeat. Recessions and bear markets will come and they will take prisoners. We’ll delve deeper into this subject and some details on the Manifest Investing Forum during August.

Bear Market Lesson? This graphic displays 10 years of prices (bottom) for the S&P 500. Relative Strength Index (top) is used as an indication of potential overvaluation (RSI>70). Major lesson from 2004-2008 was that stocks (and markets) can stay overvalued for a long time. We’re now dabbling with a momentum characteristic (ROC, middle) to see if early detection/warning is feasible. As Ken Fisher points out, in the role of The Great Humiliator, markets can stay irrational for a long time, in some cases longer than your wallet can remain solvent.

Potential Fly In The Ointment?

Mark Hulbert delivers yet another cause for concern, in addition to his trumpeting of things like low VLMAP (and our strong preference, VLLTR) levels. “We could very well be entering into a multi-decade period of much lower price-to-earnings (P/E) ratios.” (See accompanying chart. Feel free to gulp.) “That, at least, is the conclusion that emerges from a very long-term perspective on the relationship between interest rates and P/E ratios. On average since 1871, it turns out, P/E ratios have averaged just 12.8 when long-term rates have been in a secular uptrend vs. 17.5 when those rates have been in a secular downtrend.” Vulnerability can be a place where Opportunity is born. But don’t be a hero.

Mark Robertson

Mark Robertson is founder and managing partner of Manifest Investing, a source for research and portfolio management focusing on strategic long term investors.