Landauer

Solomon's Select, by Mark Robertson, Managing Partner March 1st, 2012

LDR provides technical and analytical services to determine occupational and environmental radiation exposure.

We’re always on the vanguard for an Allmon stock. One of my favorite Allmon stocks, named in honor of the “dancing bear” Charles Allmon has always been Mocon (MOCO). Allmon was notorious for (1) using undiscovered relatively small companies with large measures of consistency to build his portfolios around and (2) for those portfolios to achieve stratospheric relative returns despite a large allocation (typically 30-60% of total assets) at virtually all times to cash equivalents. We don’t know if Landauer (LDR) fits the bill but the company feels very Mocon-like, establishing a leadership position in radiation monitoring and consulting.

Landauer provides technical and analytical services to determine occupational and environmental radiation exposure. Services and equipment are provided to measure the dosages of X-ray, gamma radiation and other penetrating ionizing radiation exposure primarily through badges. The company also manufactures radiation detection monitors; distributes and collects results; and analyzes and reports exposure findings. 90% of revenues are recurring and Landauer reports the award of an incremental government contract (think FEMA) that will be material in the 2012 results.

Landauer: Chronicle. In the words of Jon Stewart, “Wait for it. Wait for it.” Landauer has been on the watch list for quite a while but as the chronicle displays, the price decline over the last several months has delivered the highest PAR and relatively high relative return of late. I wouldn’t be surprised to see this high-quality company as a resident in the Solomon Select tracking portfolio for an extended stay.

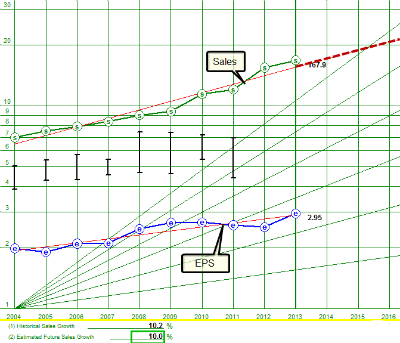

Landauer (LDR): Business Model Analysis. Some of the boost to a 10% sales growth trend shown here is a strategic acquisition. That said, the company’s revenue stream is a model of consistency.

Growth, Profitability and Valuation

Our sales growth forecast for Landauer is 10%. This is based on analyst consensus forecasts and a regression from 2004-2013.

The net margin (2007-2011) checks in at 23.5%. We’re using 22% — a median for the span 2007-2015 that recognizes that a return to 25-26% net margins is less likely with the recent acquisitions and slightly lower margins associated with the government contract.

The five year trailing average average P/E is 22.8×. Based on consensus and industry analysis, we’re assigning a projected average P/E of 21×.

At a stock price of $52.03, the projected annual return is approximately 16-17%. The quality rating is 90.6 (Excellent, top shelf) and the financial strength rating is 98 (A++).

Thursday, March 8 is worldwide Ladies Day. It may seem chauvinistic but we find it comforting these days to pull up the page of company leaders and see the Landauer leadership team populated with a number of ladies — in the case of Landauer, the participation approaches 50% and something feels right about that.

It would be quite the challenge to argue that Landauer isn’t leveraged into some of the key issues and challenges facing us now and in the years ahead. The presence in healthcare & education, energy, industry and national security speaks volumes about the sustainability of business potential for the company.

“2011 demonstrated the balance we are taking in the pursuit of new growth opportunities and managing resources effectively to produce steadily improving long-term performance in our core business and new markets,” stated Bill Saxelby, President and CEO of Landauer. “We made significant progress against our strategic priorities … and see strong interest for services that integrate our traditional business with [new areas of opportunity].”

You had us at “steadily improving long-term performance.”

Mark Robertson

Mark Robertson is founder and managing partner of Manifest Investing, a source for research and portfolio management focusing on strategic long term investors.